This week SoFi Technologies (SOFI) has gained much more spotlight, especially due to its upcoming earnings report which will be scheduled for Tuesday before the market open. We will going to see with the boost of Fin-tech and AI integration, the company result will decide the investor sentiments. If strong earning report comes, then $35 breakout is easily possible, but if the guidance becomes weak, then we may also see short-term profit booking. This report is very crucial for the SoFi because it show the reality of long-term profitability shift and product growth momentum. Many trader are also eagerly waiting to see whether SoFi will continue its rally or faces the temporary pause.

📊 SoFi’s Current Setup – Momentum Is Real

The current status of SoFi stock is, it reaches $30 per share — a level from where both the breakout and correction are possible. If you see its last 6 moths chart then you get to know that SoFi has given upto 135% of return — which is a quite massive for nay fintech stocks.

We have been personally an investor in SoFi since the sub-$10 days. We think this stock is still undervalued as because the company has multiple revenue engines and a solid execution track record. The ecosystem of SoFi has capture everything just from every core financial service area, from leading to investing and insurance — exactly where the long-term compounding always begins.

💰 Why This Earnings Could Change the Game

It is generally obvious that earning week is the make or break moment for each and every stock — and even more critical for SoFi stocks.

Key Catalysts This Quarter:

- New Revenue Stream: The launch of Option Level 1 trading is a fresh growth driver for SoFi and a best proof of revenue diversification.

- Membership Boom: With a huge number of approx 7+ million member, SoFi’s network effect is growing at an exponential speed.

- Profitability Transition: The company is finally on the verge of transforming from an nonprofit fintech to profit-generating fintech and its margin are also improving.

If the management highlight option trading adoption data and engagement metrics in the earning call option, then there may be chances that wall street sentiments could flip overnight.

Projection: Strong report = $35 likely; earnings beat = $40 push possible.

📈 Analysts – Still Late to the Party

Traditional analysts are still stuck in old valuation frameworks.

- Morgan Stanley target: $13 → $18

- JP Morgan: $24 → $26

From the current scenario, these estimates are significantly behind the current sentiments. SoFi used to trade near $30, and analyst upgrades are still stuck on the conservative side. When the market cap of SoFi is $14B, then some big analyst predicted that this company has capacity to reach $30B company. Now the next logical milestone looks like to be a $40B market cap in the near-term especially if the profit sustained.

🧠 Investment Philosophy – Fundamentals Beat Hype

Many traders in the market just decides only by looking intraday charts and Bollinger Bands, but according to us, the actual simple question is one one:

“Will company generates the durable cash flow?”

In the case of SoFi, the simple answer is — Yes. The company has omni-channel ecosystem where users manage loans, investing, cards, and insurance. Once you are in SoFi’s ecosystem, it is difficult to exit. They have built a financial “matrix” — cross-selling through AI analytics increases the profit margin with every product.

🧮 Option Trading: The Next Growth Engine

Currently, The option trading feature is a silent game-changer for many traders. Just imagine — If SoFi’s 1 million active investor start option trading, the company will get a massive revenue kick from transaction-based income. With the option features, SoFi poses direct challenges to fintech like Robinhood. If the adoption rate are high, valuation re-rating could be instant.

From the current scenario, we have seen that SoFi’s strategic move toward derivatives trading proves one thing: They’re thinking like a full-service brokerage now, not just a neobank.

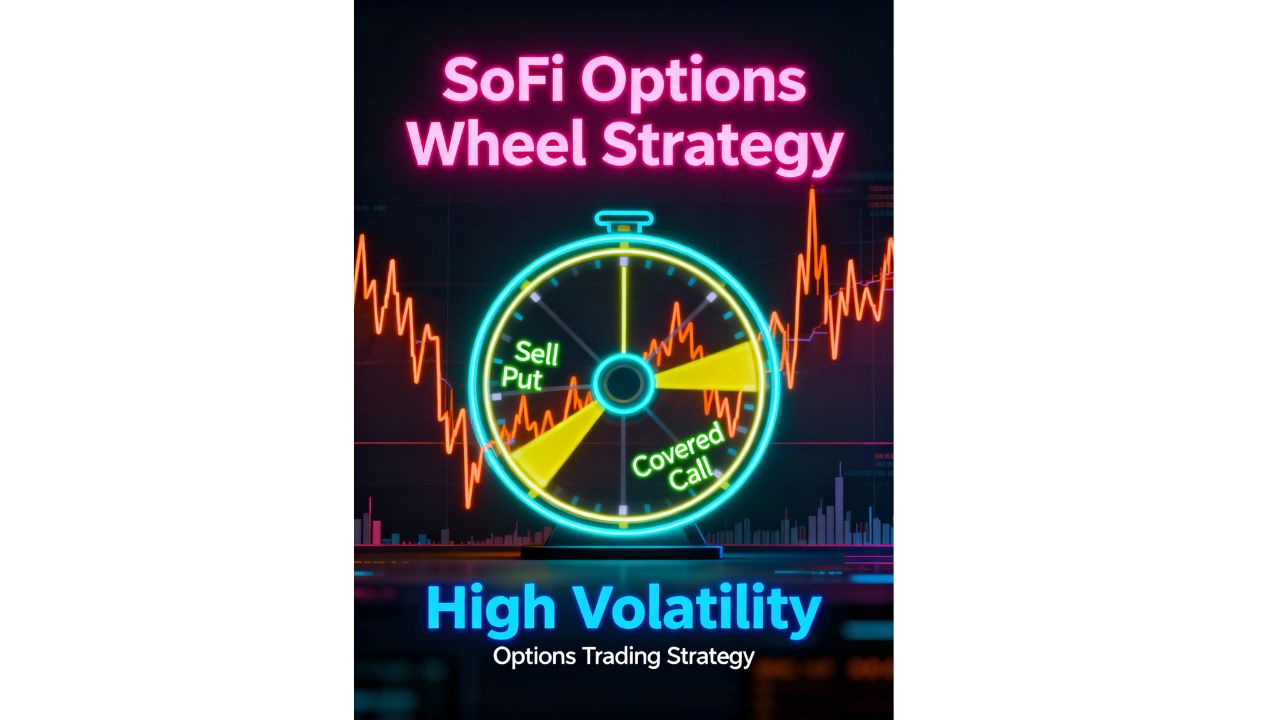

⚙️ Covered Strangle – Smart Income Strategy

For this, I would personally like to use covered strangle on SoFi for consistent monthly returns:

- Sell put options → If the stock goes down, then shares are available at lower price.

- Sell covered calls → If the stock goes up, then you will get the premium. The upside is limited, but it is safe.

Example:- I hold the share at $30 per share and sell at $35 covered call with one month expiry. Implied Volatility(IV) is currently high, so the premium is also high. A call arund the 24 delta is a best spot— with the balance of both income and upside balance.

🔍 SoFi’s Evolving Business Empire

SoFi’s business model is literally building a financial universe:

- Loans: Like Personal, student, home – all high-margin verticals.

- Investing: With the stocks, crypto, IPO access, aur ab options trading.

- Credit Cards: Cash-back aur referral-based campaigns = customer stickiness.

- Insurance: Auto, renters, life, aur homeowners coverage portfolio.

- Marketing Edge: NFL sponsorship, influencer partnerships, aur SEO dominance.

With the combination of all these segment, has created a self-sustaining growth flywheel for SoFi, where one product pushes the customer to buy another — compounding effect at its best.

💡 Long-Term Vision – From Fintech to Financial Super App

The real mission of SoFi is “One App for All Financial Needs.” There model are simple — Keep the Customer Acquisition Cost (CAC) low and keep the Lifetime Value (LTV) high.

Example: If a customer is acquire at $40 of cost and its life time value is $1,000+ — then with each and every new sign-up become a profit generator. The AI insights and cross-selling data are now making the SoFi a super app for pure financial ecosystem — where both product switching and loyalty are naturally lock-in.

📅 Price Outlook

- Short Term (3 months): $35–$40 potential if earnings beat expectations.

- Medium Term (1 year): $42–$45 probable with consistent profitability.

- Long Term (2026–27): $60+ if SoFi global expansion and execute the M&A prudently.

Even if any little pullback comes (to the $25 zone), then that could be the perfect re-entry level. The dip buying opportunities is clear.

⚠️ Risk Factors – Stay Grounded

- Earnings Miss: 10–15% probability is that the growth metric will miss.

- Competition: Square, Robinhood and big banks fintech dominance are fighting for the fintech dominance.

- Valuation Expansion: Short-term volatility is expected after doubling in 6-months.

Still, The advantage brand moat and ecosystem of SoFi protect it from isolated shocks. And the its biggest safety net is its loyal customers and wide product range.

🧾 Final Thoughts – SoFi Is Just Getting Started

After seeing all this, we can clearly says that SoFi is just not only a fintech — but a movement toward the future of finance. Volatility is possible after earning, but long-term narrative looks like extremely bullish. For the instance, If the management provides clarity on option adoption, loan growth and customer leverage, then we will be confident that $35+ rally is inevitable. For us, SoFi is a buy for dip and hold for wealth” type stock.

📢 Disclaimer: This article is for educational and informational purpose. We are not a registered financial adviser. Before taking any Investment decisions, evaluate your own research and risk tolerance.